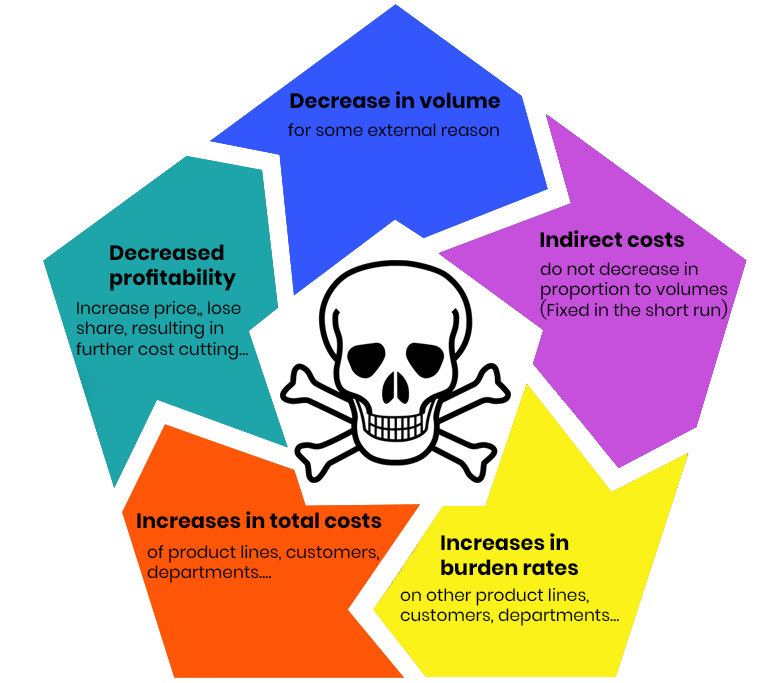

The death Spiral of cost cutting

Imagine a flight from Brussels to Nice in November. The plane isn’t full. On paper, the route is losing money. So the airline’s leadership asks the obvious question: should we cancel it?

If they do, they save on fuel, catering, and ground handling. But the pilot’s salary still gets paid. The lease on the aircraft doesn’t disappear. The gate fees continue. Cancel the flight, and those costs don’t vanish — they get redistributed across the remaining routes, making them look worse than they did before.

This is how cost-cutting spirals begin.

The Porthos Problem

Let’s make it concrete. Consider a company with three customers: Aramis, Athos and Porthos.

| Aramis | Athos | Porthos | Total | |

|---|---|---|---|---|

| Sales | 300,000 | 180,000 | 240,000 | 720,000 |

| Cost of goods sold | 216,000 | 138,000 | 198,000 | 552,000 |

| Materials handling labour | 24,600 | 10,800 | 19,800 | 55,200 |

| Materials handling equipment (depreciation) | 6,000 | 3,600 | 4,800 | 14,400 |

| Rent of warehouse | 8,400 | 4,800 | 8,400 | 21,600 |

| Marketing expenses | 5,000 | 7,000 | 6,000 | 18,000 |

| Order and delivery processing | 7,800 | 4,200 | 7,200 | 19,200 |

| General admin expenses | 12,000 | 7,200 | 9,600 | 28,800 |

| Profit | 20,200 | 4,400 | -13,800 | 10,800 |

Porthos is losing €13,800. The instinct is clear: drop Porthos, protect the bottom line.

But watch what happens next. When Porthos is removed, the fixed costs — equipment depreciation, warehouse rent, general admin — don’t disappear. They get reallocated to Aramis and Athos. The result: total profit drops from €10,800 to €1,800. Aramis, previously healthy, is now barely breaking even. Athos moves into the red.

Dropping the loss-maker made things worse.

The lesson

Cost cutting feels decisive. It rarely is, without the right analysis behind it. Before dropping a product, a customer, a department, or a route — understand what costs actually go away, what costs stay regardless, and what you give up by walking away.

Otherwise, you don’t cut your way to profitability. You spiral toward it.

Why This Happens: Relevant Costs

The mistake is treating all costs as if they respond to every decision. They don’t.

In decision-making, the only costs that matter are relevant costs — costs that actually change depending on what you decide. Equipment depreciation, warehouse rent, and general admin are fixed. Whether Porthos stays or goes, those expenses exist. They are sunk costs.

What is relevant? The costs that would genuinely disappear if Porthos left: cost of goods sold, materials handling labour, marketing expenses directly tied to that customer, order and delivery processing. Strip those out, and Porthos is generating a contribution margin of €13,800 — money that was covering a share of the fixed cost base.

Remove Porthos, and that contribution is gone. The fixed costs remain. Everyone else absorbs them.

And Don’t Forget Opportunity Costs

Before any cost-cutting decision, there is one more question: what are your alternatives?

Could the capacity freed up by dropping Porthos be redeployed more profitably? Could the customer relationship be restructured — different pricing, different service level — to improve the margin? Opportunity cost is the value of the path not taken. It rarely appears on a P&L, but it always affects one.